Patanjali’s SNAFU ( Situation normal, all fucked up)

Patanjali’s reckless growth is not as simple. CNBC reports that it is maize of hundreds of shell companies.

Patanjali’s reckless growth is not as simple. CNBC reports that it is maize of hundreds of shell companies.

Brief:

21 private companies and 26 partnerships with controlling stake.

These companies have no operations, so income. Yet they earn revenue from the interest of the bank deposits. Only four operate as business entities.

Incorporation of these firms are not clear. They have also changed their names.

The investments in these entities range from Rs 65.6 crore to a couple of lakhs of rupees.

Sample transaction:

Complex transactions reminds of the mind boggling questions of the competitive exams.

According to the company’s filings with the RoC, in January 2015, Sunita Poddar transferred almost her entire stake to her husband as a “gift”. She was left with only two shares of her own.

In March 2015, Sarwan transferred 12.52 lakh shares, again as a “gift”, to their son Deepak.

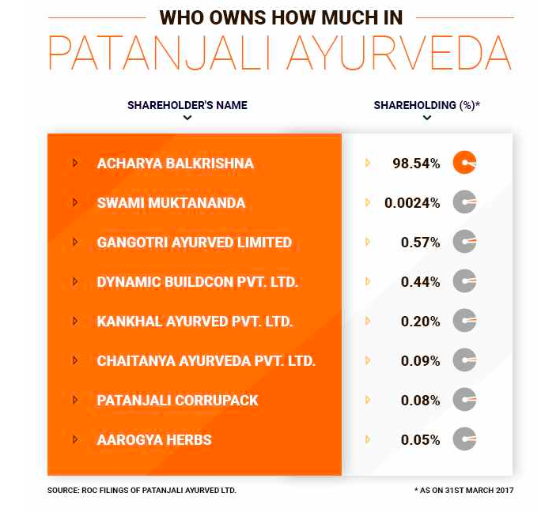

The very same day, Deepak transferred the gifted shares to Balkrishna (1.44 lakh shares),’s brother Ram Bharat (5.96 lakh shares), Gangotri Ayurveda Ltd (2.37 lakh shares), Kankhal Ayurveda Pvt Ltd (84,032 shares), Chaitanya Ayurveda Ltd (39,854 shares), Sneh Bharat (11,290 shares), Dynamic Buildcon Pvt. Ltd (83,870 shares), Patanjali Corrupack Pvt Ltd (33,119 shares) and Aarogya Herbs (India) Pvt Ltd (22,580 shares).

NDBJ Insight:

I am not saying it’s a ponzi scheme, but the characteristics are similar. A year ago it was profitable. A year later it hasn’t produced profit. It has also stopped growing. FMCG brands take years of hard work to build.

Overnight success of Patanjali is questionable. What is more worrying is the financing of the business. Only brands such as Amazon or Ambani have access to unlimited capital, only after they have proved they mettle in their businesses in the past.

Recommended reading:

- From Baba to Lala